The Role of Growth Strategies in Acquisitions

with Fred Bereskin, Micah Officer, and Jing Wang

Journal of Corporate Finance, Forthcoming

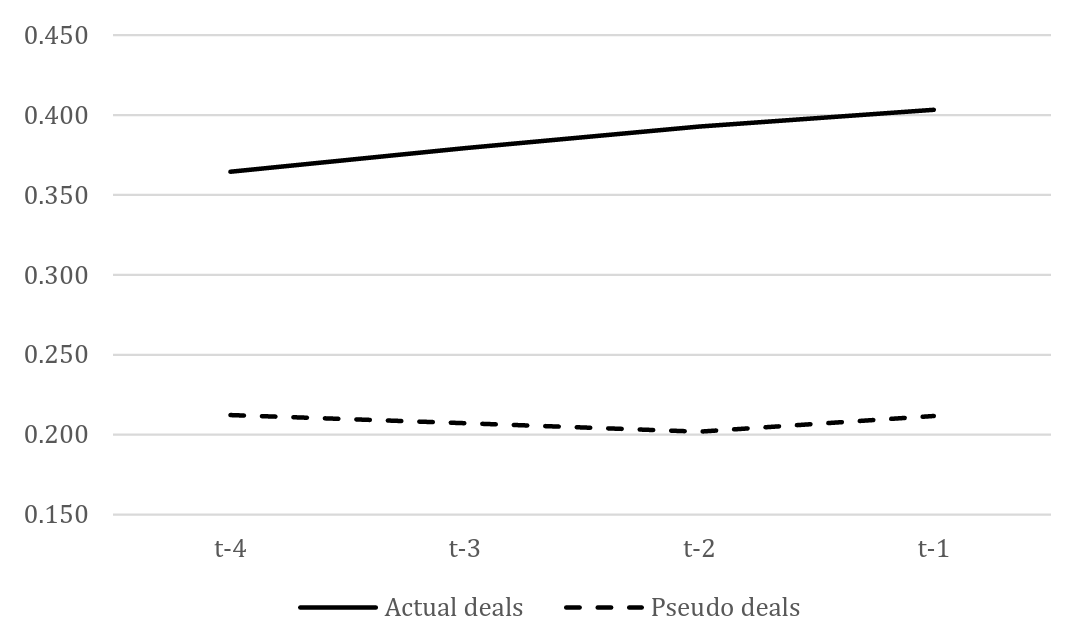

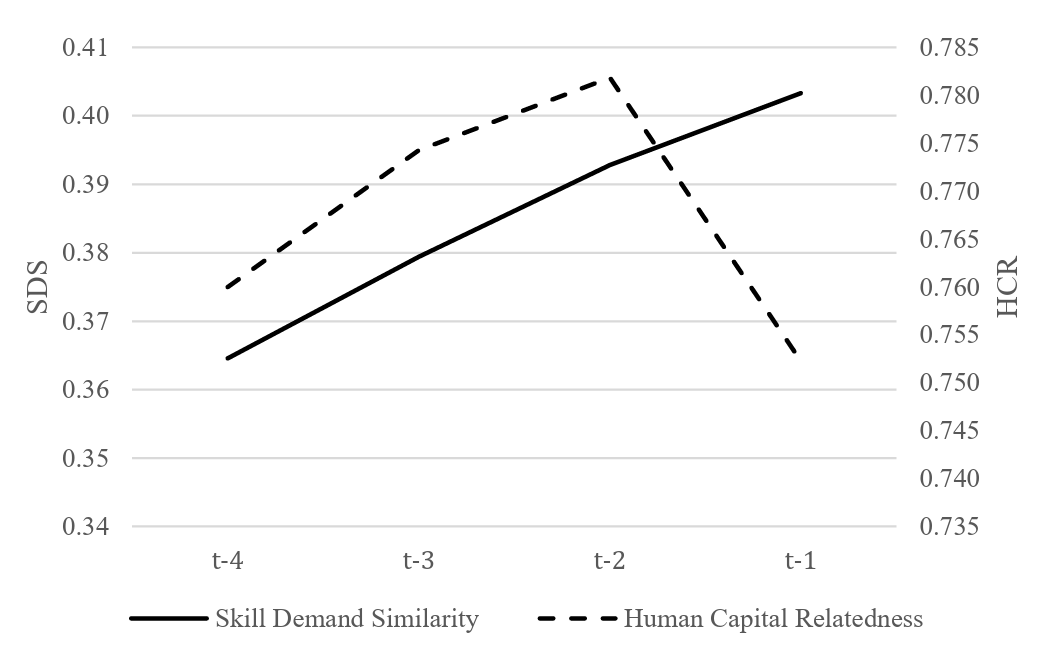

Using labor skill demand disclosed in job postings as a proxy for firms' growth strategies, we find that similar growth strategies increase the likelihood of two firms merging. In particular, a firm is more likely to become a target as its labor skill demand becomes more similar to that of its potential acquirer. Similar growth strategies ameliorate post-merger integration challenges in facilitating merger deals. Following the merger, the combined firm continues hiring the same skills, consistent with the growth strategy persisting. These types of mergers experience more synergies and superior operating performance.